Product memo

Individuals and founders in Brazil gain clarity on their spending and savings with an automated personal finance manager. It integrates with Open Finance to pull all bank accounts, cards, and investments into a single view. AI categorizes transactions, giving users a clear, visual dashboard to track finances and spot savings opportunities.

For who

Individuals and founders in Brazil

Solves what

Automates personal finance management, providing clarity on spending and savings.

- AI transaction categorization

- Open Finance bank integration

- Consolidated financial dashboard

In their own words

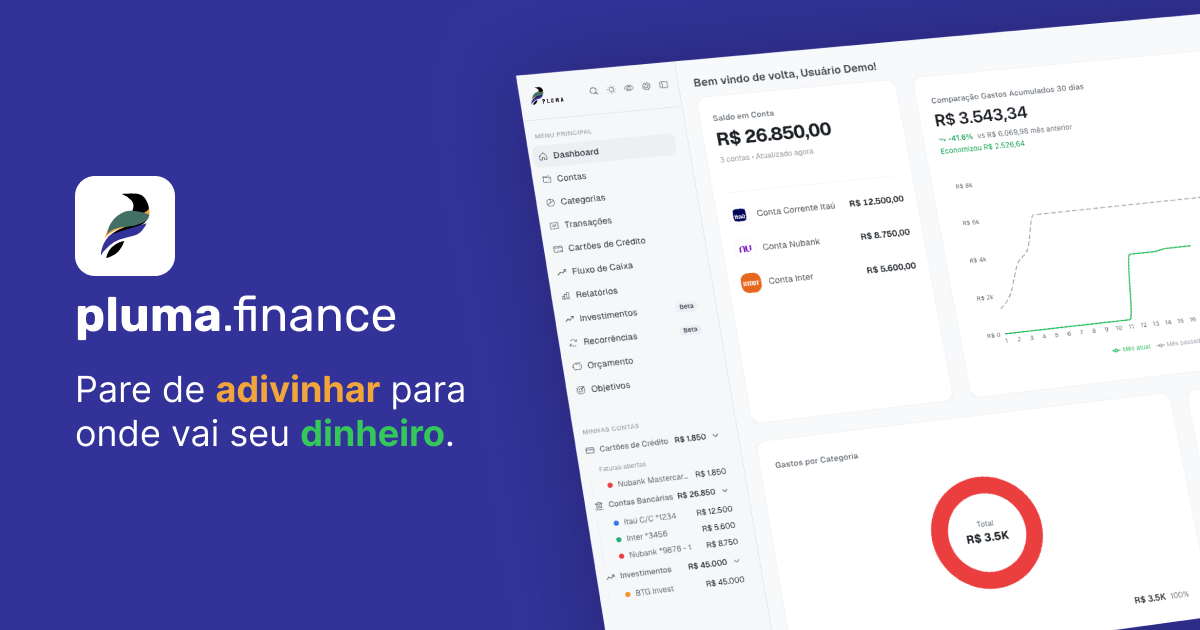

Pare de adivinhar para onde vai seu dinheiro.

Conecte Nubank, Itaú, Inter e +100 bancos em 2 minutos. A IA categoriza tudo e mostra exatamente onde você pode cortar.

Pluma automatically gathers all your accounts, cards, and investments into a simple and visual dashboard, providing clarity, security, and zero effort.

Commercial cues

Model

subscription

Free tier

No

Trial

No

Pricing Strategy

- • A 7-day trial lets users test the full experience before committing.

- • Plus adds Up to 10 accounts cards.

Operator context

Operating setup

Founded

Aug 2025

HQ

Brazil

Platform

Web app

Audience

Consumers

Payments

Stripe

Detected via TrustMRR

Social footprint

Tech stack

Market demand

Pluma keyword demand

5 keywords

Market demand is Starter-tier market intelligence.

Derived from this product’s latest SimilarWeb keyword mix — directional demand, not proof.

Builder Strategy

- Strategy Type

- Niche Specialist

- Stage

- Vc Growth

- Effort

- Solo Buildable

About Pluma Expand

Pluma provides automated personal finance management for individuals and founders in Brazil. It simplifies money tracking by integrating with Open Finance, pulling all bank accounts, credit cards, and investments into one consolidated dashboard.

The platform uses AI to categorize transactions, helping users understand their spending patterns and identify areas for saving. This focus on automated clarity and security helps reduce financial stress, making it easier for users to manage their money without constant manual input.

Pluma's tiered subscription model caters to different user needs, from basic account tracking to broad financial oversight with sharing capabilities.